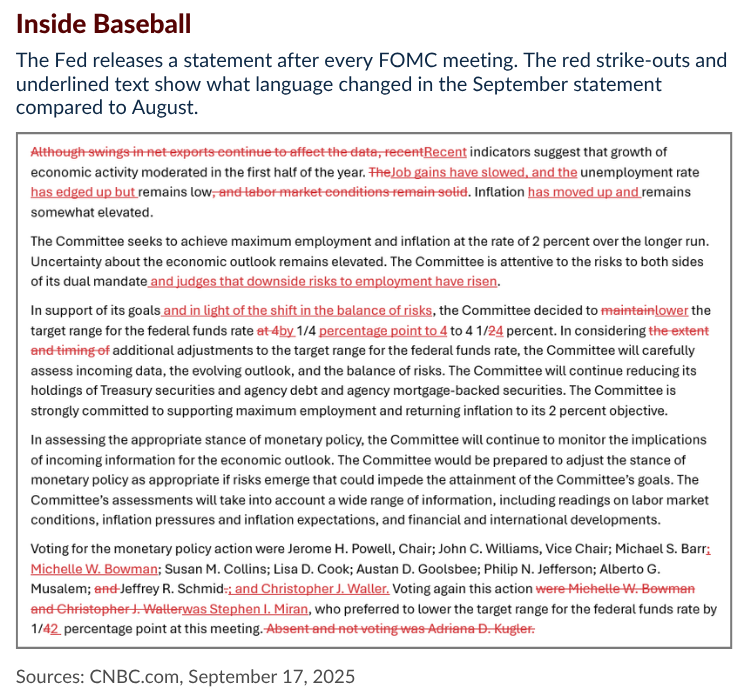

The Fed lowered short-term interest rates at its September 2025 meeting, but the question on most people’s minds is, “What’s in it for me?” That’s a fair question to ask, so here are some things to consider.

First-Wave Changes

Any loan considered “variable rate” can be expected to adjust relatively quickly, as with a home equity line of credit (HELOC). However, don’t get too excited. The change is likely to be relatively small.

Second-Wave Changes

If you’re buying a home, the Fed’s change may affect your mortgage rate. If you’re refinancing, you may also see rates change. If you’re shopping for a new car, you may see new advertised rates on car loans.

Long-Term Changes

Credit card companies might adjust their interest rates, but it may take several payment cycles before you see any movement. Remember, if you have a fixed-rate mortgage, the interest rate will not change unless you refinance or sell your home.

What’s Next?

The Fed’s decision to cut rates in September signaled a shift in the central bank’s monetary policy, as it was the first time in months that the benchmark rate has been lowered. Fed Chair Jerome Powell indicated that more adjustments were likely to come this year and into 2026 to address economic concerns, including a sluggish labor market.

So, while you may see a few benefits in the short term, more opportunities may present themselves in the longer term. If you have any questions about the Fed’s decision or what’s next for interest rates, please don’t hesitate to reach out.