Key Takeaways

● Teach through real decisions, not lectures: Give teens responsibility with clear limits so they learn from real trade-offs.

● Frame choices instead of funding purchases: Focus conversations on priorities and opportunity cost, not affordability alone.

● Use structure, and don’t rescue: Budgets only teach when boundaries are consistent, and consequences are allowed.

● Introduce investing early and revisit it periodically: Emphasize ownership, purpose, and long-term thinking over short-term results.

● Connect earned income to future goals: Encourage saving or investing part of what they earn to build accountability.

● Gradually shift from control to guidance: Keep the structure, expand the choices, and become a sounding board over time.

If you are a parent of a teen or young adult, how do you teach them to make confident money decisions before the stakes are high?

Teaching teens and young adults about money is less about formal instruction and more about repeated exposure to real trade-offs. Financial literacy develops when young people are allowed to make choices, experience outcomes, and reflect on what happened.

Parents and increasingly grandparents who play an active role in their grandchildren’s lives are often surprised to learn that the most durable money lessons do not come from lectures, apps, or classroom instruction. They come from everyday decisions involving spending, saving, and investing.

The emphasis is on structure, boundaries, and consistency rather than control. The objective is not to eliminate mistakes, but to allow learning in a lower-stakes environment while you remain as a backstop.

Why Does Financial Literacy for Teens Need to Start With Behavior, Not Theory?

Financial literacy is most effectively absorbed when you link it to behavior, because money decisions are both emotional and analytical. Teens can often explain what a budget, an investment, or interest is long before they understand how it feels to choose between competing priorities or live with the outcome of a decision.

Behavior-based learning connects money to values, trade-offs, and consequences. When teens make real decisions with real limits, abstract concepts like opportunity cost, delayed gratification, and risk tolerance become tangible. This approach also respects the intelligence of young people by engaging them as decision-makers rather than passive recipients. You need to find a happy medium that can help shape their relationship with money for years to come.

How Can You Use Everyday Spending to Teach the Value of Money?

Everyday spending becomes a powerful teaching tool when you shift from funding purchases to framing choices. Instead of focusing on whether an item is affordable, the conversation becomes whether it is worth prioritizing relative to other needs or wants.

A practical example is the back-to-school or college shopping trip. Rather than hitting the stores with a credit card, provide a fixed amount of cash and explain that they can keep any unused funds. This simple structure immediately reframes the experience. Teens see that spending less has a direct benefit and that choosing one item could mean forgoing another.

This method also introduces the concept of boundaries. The amount of cash is fixed; the decision and the outcome are theirs. Over time, this consistency builds internal discipline. If you implement this approach, stand firm and do not use a credit card to cover a shortfall.

What Does a Monthly Budget Teach That Allowances Often Do Not?

A comprehensive budget teaches sequencing, forecasting, and prioritization. A basic allowance rarely addresses these skills. When a monthly amount must cover everything from everyday basics to special events, teens must think beyond immediate wants.

One effective approach is to assign a specific clothing budget that your child must use to cover all related expenses, including underwear, athletic uniforms, shoes, and formal wear. You can assist at the outset by helping them create a list of anticipated needs, estimate costs, and map those expenses to specific months.

The most important element is restraint. If a teen spends heavily early in the year and later lacks funds for an expected event, the discomfort becomes the lesson. Experiencing the consequence of a poor choice, while inconvenient, is far more instructive than being shielded from it. You may be surprised by how quickly teens adapt once they realize trade-offs are real and consistent.

How Can Parents Introduce Investing Concepts at an Early Age Without Oversimplifying?

Investing concepts can be introduced early by anchoring them to money that feels meaningful to the child. Funds received during milestone events, such as a Bar Mitzvah at age 13, a Sweet 16 party, or a high school graduation, often provide a natural entry point.

Rather than allowing these funds to sit passively in a bank account or be spent rashly, you can possibly involve your children in opening an investment account. The emphasis should be on understanding what is owned, why it was chosen, and how it can connect to longer-term goals.

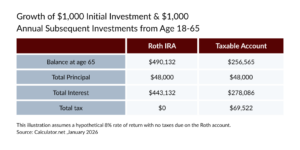

For example, if your child opens a Roth IRA at age 18 with a $1,000 initial investment from a part-time job and adds just $1,000 per year thereafter, assuming a hypothetical 8 percent average annual return, the account would be worth nearly $500,000 when your child turns 65. Remember, Roth IRA contributions are made with after-tax dollars so there are no taxes on qualified distributions in retirement.1

Remember, to qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a 5-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawals can also be taken under certain other circumstances, such as the owner’s death. The original Roth IRA owner is not required to take minimum annual withdrawals.

If your child doesn’t think they can put away $1,000 a year, remind them that skipping the daily Frappuccino might save them more than that amount.

Revisiting your child’s portfolio once a year can reinforce these lessons. Periodic reviews create familiarity with market movements and can help show the effects of market volatility. Over time, children learn that investing is not about constant activity, but about patience, ownership, and long-term thinking.

As financial professionals, we often help our clients get the next generation off to the right start in their investment journey.

What Role Can Earned Income Play in Teaching Long-Term Responsibility?

Earned income carries a different psychological weight than gifted money. When teens earn money through summer jobs, part-time work, or self-directed efforts, they can develop a stronger sense of ownership and accountability.

You can encourage your teens to contribute a portion of their earned income to their investment accounts and reinforce the habit by matching those contributions. This structure introduces multiple concepts simultaneously, including delayed gratification and the impact of compounding over time.

The framing matters. Contributions are presented as a choice with ongoing implications, not an obligation. Over time, teens begin to associate work with future flexibility rather than immediate consumption alone.

How Can Parents Teach Opportunity Cost Without a Formal Lesson?

Opportunity cost becomes clear when money is limited, and choices are visible. You can reinforce this concept by simply talking about trade-offs in everyday decisions.

For example, when your teen considers spending most of their monthly budget on a single item, you can ask what that choice means for other upcoming needs. The goal is not to discourage the purchase, but to help guide a decision that is informed.

Encouraging comparison shopping further strengthens value assessment. Asking teens to compare alternatives based on price, quality, and longevity helps them realize that the cheapest option isn’t always the least costly in the long run. At the same time, they might understand that a designer brand may not be worth the extra expense. These are important ideas children may never consider if everything is handed to them.

Why Is It Important to Allow Teens to Make Financial Mistakes?

Mistakes are essential to learning because they create emotional memories. A poor decision that leads to inconvenience or disappointment is far more likely to influence future behavior than a hypothetical warning.

Allowing mistakes requires you to show restraint. It can be uncomfortable to watch a teen struggle with the outcome of a choice, especially when the solution seems obvious. However, stepping in too quickly removes the lesson. As long as consequences are manageable and not harmful, experiencing them can build resilience and judgment that your child can use in later life.

How Can You Model Healthy Money Behavior Without Being Rigid?

You don’t have to tell your teenage children how much you make or what’s in your retirement plan, but money shouldn’t be a taboo subject either. Some might find the topic uncomfortable, but talking honestly about money can help you pass along your values and hard-won lessons from your own life. It’s almost a disservice not to discuss financial matters with your teens.

Teens learn as much from observation as from direct experience. Parents who discuss their own financial decisions in a measured, factual way provide a powerful example.

This can include explaining why a purchase was delayed, how priorities were weighed, or why saving or investing took precedence over spending. Transparency, without oversharing, helps normalize financial decision-making and manage anxiety around money.

What Strategies Can Help Young Adults Transition From Parental Structure to Independence?

As teens become young adults, the financial structure you’ve developed should evolve, not disappear. Gradually increasing responsibility allows skills to develop.

If you have a college student, you might shift from covering expenses directly to providing a fixed periodic amount that covers specific categories.

For young adults entering the workforce, conversations can expand to include benefits, saving rates, early investing in employer-sponsored accounts, and lifestyle trade-offs. Your role becomes less about control and more about serving as a sounding board.

What Should Your Child Know Before Choosing and Heading to College?

One of the most consequential events in your teen’s young life is choosing a college. It is also the time for a financial lesson. You should consider having “the talk” to set expectations about costs, trade-offs, and what you can realistically afford before your child falls in love with a college. It may not be an easy discussion, but it is necessary and potentially character-building.

Once the decision is made, going off to college may be your child’s first experience with the real world of finance, and you may want to get them ready. The goal isn’t to make them financial professionals, but to give them confidence, context, and a few hopefully durable habits.

Here are eight areas worth covering:

1. How Money Actually Flows

They should understand where money comes from, where it goes, and how quickly it can disappear. Review paychecks, bank accounts, and how tuition, housing, and everyday spending are funded.

2. Budgeting as a Decision Tool (Not a Restriction)

Teach them to track spending and look ahead, especially for irregular costs. Emphasize that a budget reflects priorities and is about trade-offs, not deprivation.

3. Credit Basics and the Cost of Debt

Explain how credit cards work, how interest compounds, what a credit score is, and why minimum payments wind up being expensive over time. One early spending mistake can linger.

4. Saving and Investing Early, Even in Small Amounts

Show them the power of starting early, whether it’s an emergency fund or a first investment account. Consistency matters more than size at this stage.

5. Financial Independence and Consequences

Talk through what expenses they are responsible for versus what you will cover. Clear boundaries reduce confusion and teach accountability.

6. Protecting Themselves Financially

Talk about scams, identity theft, overdraft fees, subscriptions, and the importance of monitoring accounts. Financial literacy today should include digital literacy and awareness of the risks of oversharing on social media.

7. Understanding Financial Transaction Apps

If your child does not use money transfer apps, this may be a good time to start. In our increasingly cashless society, apps are often used to handle finances, such as splitting a restaurant bill or a rideshare with friends. Explain how they work and the pros and cons.

8. Asking Questions and Seeking Help

Encourage your children to ask your opinion before making big financial decisions. Knowing when to pause and ask is a skill in itself.

Why Does Financial Literacy Build Confidence Beyond Money?

Understanding money strengthens broader life skills, including problem-solving, self-control, and long-term thinking. Teens who feel financially capable often carry that confidence into career choices, relationships, and life decisions.

By engaging with real numbers and real consequences early, young people learn that financial decisions are manageable rather than overwhelming.

How Can You Balance Guidance With Autonomy Over Time?

The balance shifts gradually. Early on, you provide more structure and fewer choices. Over time, the structure remains, but the choices expand.

The most effective approach is iterative. You can observe how your teen responds, thoughtfully adjust boundaries, and maintain open communication. The objective is not perfection, but progress.

What Does Effective Financial Education at Home Ultimately Look Like?

While 30 states now require high school students to take a standalone personal finance course of at least one semester before graduation, there is no substitute for what they can learn about the subject at home.2

Effective education is quiet and cumulative. It shows up in thoughtful questions, restrained spending, and an ability to articulate priorities.

It is rarely about mastering terminology or pursuing ideal outcomes early. Instead, it is about developing judgment through experience, reflection, and consistency.

How Can Families Continue These Conversations as Circumstances Change?

Money conversations should evolve alongside life stages. What begins with clothing budgets and gift money can later include discussions about housing choices, career paths, and life commitments.

Keeping the dialogue open reinforces that financial decision-making is ongoing and adaptable. It also signals respect for the growing independence of young adults.

In the final analysis, the most effective teaching happens when parents and grandparents create space for ownership while remaining available as a resource.

We Are Here for You

As financial professionals, we can help you frame these conversations or give you our thoughts on different approaches.

Remember, financial education is an ongoing process, so don’t be afraid to seek guidance. Helping children develop good financial habits early in life can set them on a path toward a healthier relationship with money.

Sources: