There are a lot of tax changes tucked in the nooks and crannies of the 800+ page One Big Beautiful Bill Act (OBBBA) passed earlier this month. One that you may have heard about created a $10,000 tax deduction when you finance a new car.

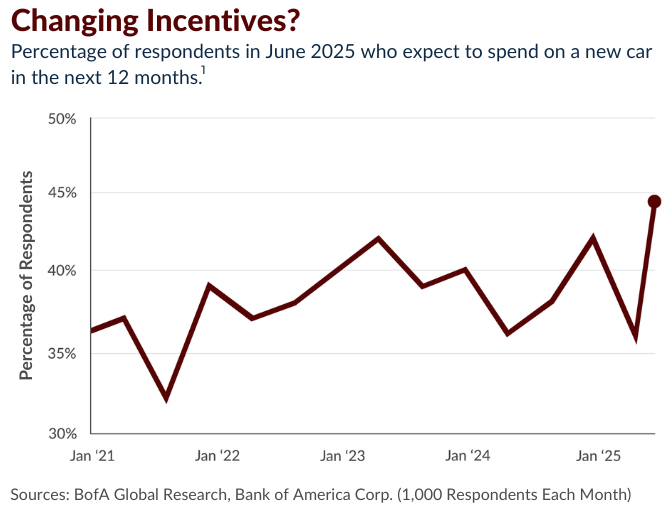

As you can see in the chart below, in June, many Americans were already showing interest in buying a new car. So, will this new tax incentive inspire even more people to visit the showroom?

Let’s start by breaking down how the new tax rule works. Starting this year, you can deduct up to $10,000 of interest on new auto loans from your income. To qualify, the car must be brand-new and final assembly of the vehicle must take place here in the U.S.

The deduction phases out for single filers with modified adjusted gross income of $100,000 and $200,000 for married couples filing jointly. Be sure to consult with a tax professional to determine if you are eligible and whether this deduction could apply to your specific tax situation.2

While today’s car buying trends may connect to recent news, it’s another reminder that there are more ways to measure the economy than following job updates, inflation reports, and Fed meetings.

It’s important to also keep an eye on other trends like “the number of people who expect to buy a new car” as it can provide insight on current consumer confidence levels. After all, most people will only consider a new car when they feel good about their finances—and the future.

If you have questions about the OBBBA and how it might impact your financial strategy or goals (such as buying that new car), please don’t hesitate to reach out.

1BofA Global Research, Bank of America Corporation, June 2025.

2IRS.gov, July 14, 2024. “One Big Beautiful Bill Act: Tax deductions for working Americans and seniors”