You might be asking yourself, “Who is TINA? And why would they be managing my money?” TINA is an acronym that stands for “There is No Alternative” to stocks. For most retirement-minded investors, “TINA” could be considered their money manager.

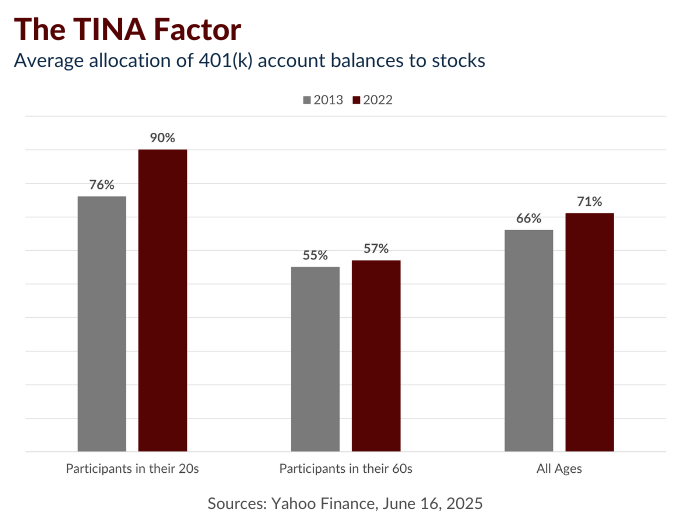

As the chart below indicates, 71% of 401(k) account balances were allocated to stocks in 2022. People in their 60s had slightly less allocated to stocks, while participants in their 20s were almost exclusively in equities.1

It’s difficult to argue against the strategy, especially for someone in their 20s. Since 1957, the Standard & Poor’s 500 index has delivered an annual return of more than 10%. But patience, focus, and commitment are required. The path since 1957 has been anything but smooth, with recessions, global crises, and geopolitical events all taking place along the way.2,3

Thus, the question remains: for people who are approaching retirement, should TINA be managing their money?

It’s possible, but there are many other factors to consider when a person stops accumulating assets and starts spending those assets that they have spent a lifetime accumulating. Not to mention accounting for how Social Security factors into the equation.4

When we create a financial strategy for our clients, we allocate assets based on their personal goals, risk tolerance, and timeline. So, TINA will likely be part of those conversations, but is certainly not the only voice in the room.

If you have questions about TINA’s role in your overall financial strategy or would like to revisit your retirement plan, please feel free to reach out.

1Yahoo Finance, “The Stock Market’s Secret Weapon: Insatiable Demand from American Retirement Accounts.” June 16, 2025.

2Investopedia.com, “S&P 500 Average Returns and Historical Performance.” May 16, 2025.

3The S&P 500 Composite Index is an unmanaged index that is considered representative of the overall U.S. stock market. Index performance is not indicative of the past performance of a particular investment. Past performance does not guarantee future results. Individuals cannot invest directly in an index. The return and principal value of stock prices will fluctuate as market conditions change. And shares, when sold, may be worth more or less than their original cost.

4Once you reach age 73, you must begin taking required minimum distributions (RMDs) from your 401(k) or any other defined contribution plan in most circumstances. Withdrawals from your 401(k) or any other defined contribution plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.