If you have ever taken a close look at a U.S. dollar note, each bill has the words “Federal Reserve Note” imprinted across the top. But why are these notes issued by the Federal Reserve and what role does it play in the U.S. economy?

The Federal Reserve, commonly referred to as “the Fed,” serves as the central bank of the United States. Established by Congress in 1913, its purpose is to ensure a safer, more adaptable, and stable monetary and financial system. Prior to its inception, the U.S. economy faced frequent episodes of panic, bank failures, and limited credit availability.1

As it stands today, the Fed has four main roles in the U.S. economy:

1. Monitor the Economy

In addition to its other duties, the Fed is responsible for three primary mandates within the economy: maximizing employment, stabilizing price levels, and maintaining moderate long-term interest rates.1

Keep in mind that although the Fed cannot directly control employment, inflation, or long-term interest rates, it utilizes various tools at its disposal to influence the availability and cost of both money and credit. This, in turn, influences the willingness of consumers and businesses to spend on goods and services.

For example, when the Fed lowers short-term interest rates, borrowing money becomes cheaper, encouraging consumers to spend more. Increased consumer spending can stimulate economic growth, prompting companies to expand production and employment. When short-term rates are low, the Fed closely monitors economic activity to watch for signs of inflation.

Conversely, when the Fed raises short-term rates, borrowing costs increase, reducing consumer spending motivation. This effect can slow economic growth and lead companies to scaling back on production and reducing their workforces. When short-term rates are elevated, the Fed must watch for signs of a decline in overall price levels.

2. Supervise and Regulate

The Fed establishes and enforces regulations that banks, savings and loans, and credit unions must follow. It collaborates with other federal and state agencies to ensure these financial institutions remain financially sound and that consumers receive fair and equitable treatment. If an organization encounters issues, the Fed exercises its authority to mandate corrective actions.

3. Maintain Stability

The Fed helps uphold the stability of the U.S. financial system by providing payment services. During periods of financial stress, it is able to serve as a lender of last resort, supplying liquidity to either a specific bank or the entire banking sector. For example, the Fed may purchase government bonds from a particular bank in order to provide it with the necessary funding to carry out its operations.

4. Banker for Banks, U.S. Government

The Fed offers financial services to both banks and other depository institutions, as well as directly to the U.S. government. For financial institutions like banks, savings and loans, and credit unions, it manages accounts and provides various payment services, including check collection, electronic funds transfers, and the distribution of new currency while also handling the removal and destruction of old, worn-out currency. For the federal government, the Fed is responsible for paying Treasury checks, processing electronic payments, and overseeing the issuance, transfer, and redemption of U.S. government securities.

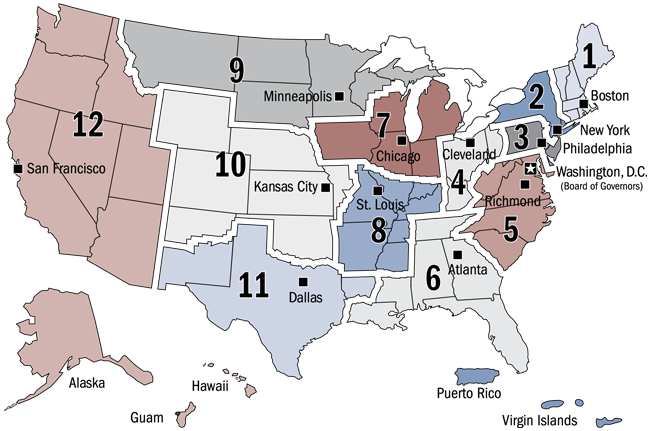

A Decentralized Central Bank: Why It Works

The Federal Reserve System consists of 12 independent banks that operate under the supervision of a federally appointed Board of Governors based in Washington, D.C. Each of these banks oversees its own specific district, as shown in the chart below.

Source: Board of Governors of the Federal Reserve System

This structure ensures regional representation and offers a more accurate reflection of the diverse economic conditions across the country. With oversight from a Board of Governors, the system strikes a balance between regional operations and centralized decision-making, enhancing adaptability and responsiveness while maintaining stable monetary policy.

1FederalReserve.gov, 2024.