Traditional Individual Retirement Accounts (IRA), which were created in 1974, are owned by roughly 36.6 million U.S. households. And Roth IRAs, created as part of the Taxpayer Relief Act in 1997, are owned by nearly 27.3 million households.1

Both are IRAs. And yet, each is quite different.

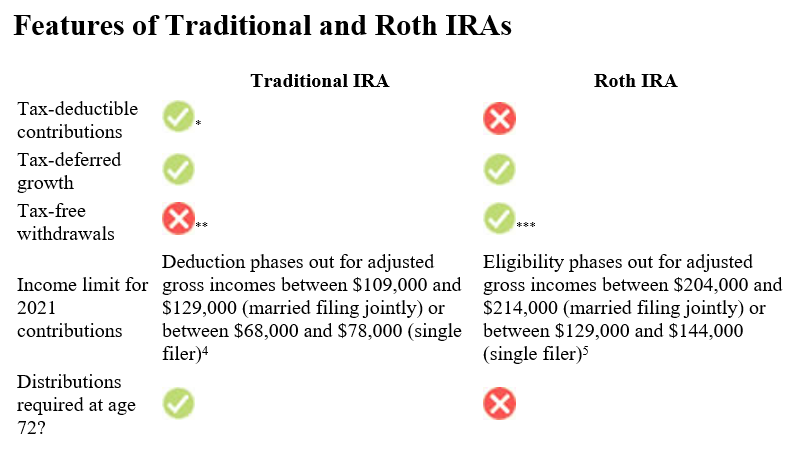

Up to certain limits, traditional IRAs allow individuals to make tax-deductible contributions into their account(s). Distributions from traditional IRAs are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 72, you must begin taking the required minimum distributions.2,3

For individuals covered by a retirement plan at work, the deduction for a traditional IRA in 2022 is phased out for incomes between $109,000 and $129,000 for married couples filing jointly, and between $68,000 and $78,000 for single filers.4

Also, within certain limits, individuals can make contributions to a Roth IRA with after-tax dollars. To qualify for a tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½.

Like a traditional IRA, contributions to a Roth IRA are limited based on income. For 2022, contributions to a Roth IRA are phased out between $204,000 and $214,000 for married couples filing jointly and between $129,000 and $144,000 for single filers.4

In addition to contribution and distribution rules, there are limits on how much can be contributed each year to either IRA. In fact, these limits apply to any combination of IRAs; that is, workers cannot put more than $6,000 per year into their Roth and traditional IRAs combined. So, if a worker contributed $3,500 in a given year into a traditional IRA, contributions to a Roth IRA would be limited to $2,500 in that same year.4

Individuals who reach age 50 or older by the end of the tax year can qualify for “catch-up” contributions. The combined limit for these is $7,000.4

Both traditional and Roth IRAs can play a part in your retirement plans. And once you’ve figured out which will work better for you, only one task remains: open an account.5

* Up to certain limits

** Distributions from traditional IRAs are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 72, you must begin taking the required minimum distributions.

*** To qualify, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½.

1ICI.org, 2022

2IRS.gov, March 12, 2021. Under the SECURE Act, in most circumstances, once you reach age 72, you must begin taking required minimum distributions from a Traditional Individual Retirement Account (IRA). You may continue to contribute to a Traditional IRA past age 70½ under the SECURE Act as long as you meet the earned-income requirement.

3Up to certain limits, traditional IRAs allow individuals to make tax-deductible contributions into their account(s). Distributions from traditional IRAs are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 72, you must begin taking the required minimum distributions.

4IRS.gov, 2022

5The Tax Cuts and Jobs Act of 2017 eliminated the ability to “undo” a Roth conversion.