Procrastination is something most of us have experienced at some point in our lives. In some instances, it may seem harmless—putting off a task until tomorrow. However, delaying certain decisions can eventually catch up with us in unexpected ways.

Imagine you’re driving along when a police cruiser pulls up behind you with its lights flashing. You pull over, the officer gets out, and your heart drops as they say, “Did you know that your registration has expired?” Instead of spending a few minutes renewing it online, you’re now facing a hefty ticket. What you thought was a minor delay has turned into a costly mistake.

Procrastinators often self-sabotage themselves, creating unnecessary obstacles that hinder progress. This can result in missed deadlines, missed opportunities, or just plain missing out—especially when it comes to your financial strategy.

Why Delaying Financial Decisions Can Cost You

Mark Twain famously quipped, “Never put off until tomorrow what you can do the day after tomorrow.” But in reality, procrastination can be detrimental to both our personal and professional lives. So, why do we do it?

The reasons why people procrastinate have been widely theorized, and there is an entire industry of books, articles, videos, and workshops dedicated to helping people overcome it. Interestingly enough, simply acknowledging the cost of putting off certain tasks or decisions can be a powerful motivator to take action sooner rather than later.

Regardless of the psychology behind it, procrastination can end up costing you valuable time—and money.

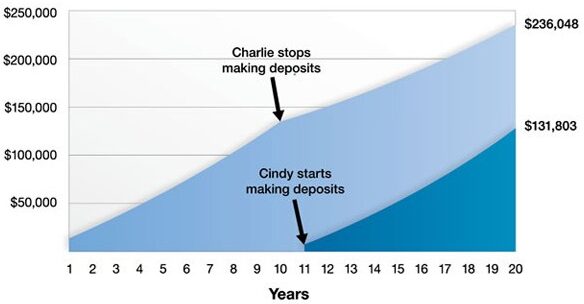

Early Bird Gets the Worm

To help illustrate the cost of delaying your investment strategy, consider this hypothetical example about Cindy and Charlie, who each invest $100,000 over a 10-year period.1

Charlie immediately begins depositing $10,000 a year into an account that earns a 6% rate of return. Then, after 10 years, he stops making deposits.

Cindy, on the other hand, waits 10 years before getting started. She then starts to invest $10,000 a year for 10 years into an account that also earns a 6% rate of return.

After 20 years, Cindy and Charlie have both invested the same amount, but Charlie’s balance is much higher because his account has had more time for the investment returns to compound.1

Take Action

Don’t let procrastination derail your financial future. If you’ve put off creating an investment strategy or updating your financial plan, the good news is that it’s never too late to start. Small actions taken today can make a big difference down the road.

1This is a hypothetical example of mathematical compounding. It’s used for comparison purposes only and is not intended to represent the past or future performance of any investment. Taxes and investment costs are not considered in this example. The results are not a guarantee of performance or specific investment advice. The rate of return on investments will vary over time, particularly for long-term investments. Investments that offer the potential for high returns also carry a high degree of risk. Actual returns will fluctuate. The type of strategies illustrated may not be suitable for everyone.