When it comes to planning for retirement, understanding the savings options available to you is an important first step. While many people are familiar with traditional 401(k) plans, others may not be as acquainted with Roth accounts.

Leveraging alternative savings options such as a Roth 401(k) may offer benefits that align better with your retirement goals and timeline. Whether you’re deciding how to allocate contributions or debating the tax advantages, let’s take a closer look at the benefits of Roth 401(k)s and how they work.

What Are the Benefits?

Since 2006, employers have been allowed to offer workers access to Roth 401(k) plans. As the name implies, Roth 401(k) plans combine features of 401(k) plans with those of a Roth IRA. Unlike a traditional 401(k), contributions are made with after-tax dollars, meaning when you are ready to take qualifying withdrawals in retirement, they are tax-free—including any accrued growth earned along the way.1,2,3

Roth 401(k) plans also are not subject to income restrictions like Roth IRAs are. This can offer a unique advantage to high-income individuals whose Roth IRA has previously been limited by these restrictions.

Please remember that this article is for informational purposes only and is not a replacement for real-life advice, so be sure to consult with a tax or financial professional before considering any adjustments to your retirement strategy.

Roth 401(k) vs. Traditional 401(k): How to Choose

Deciding between a Roth 401(k) and a traditional 401(k) often comes down to whether you value the immediate benefit of reducing your taxable income today or would rather enjoy the tax-free savings and withdrawals in retirement. Often, this is not an “all-or-nothing” decision as many employers allow contributions to be divided between a traditional 401(k) plan and a Roth 401(k) plan as long as you stay within the annual contribution limits.

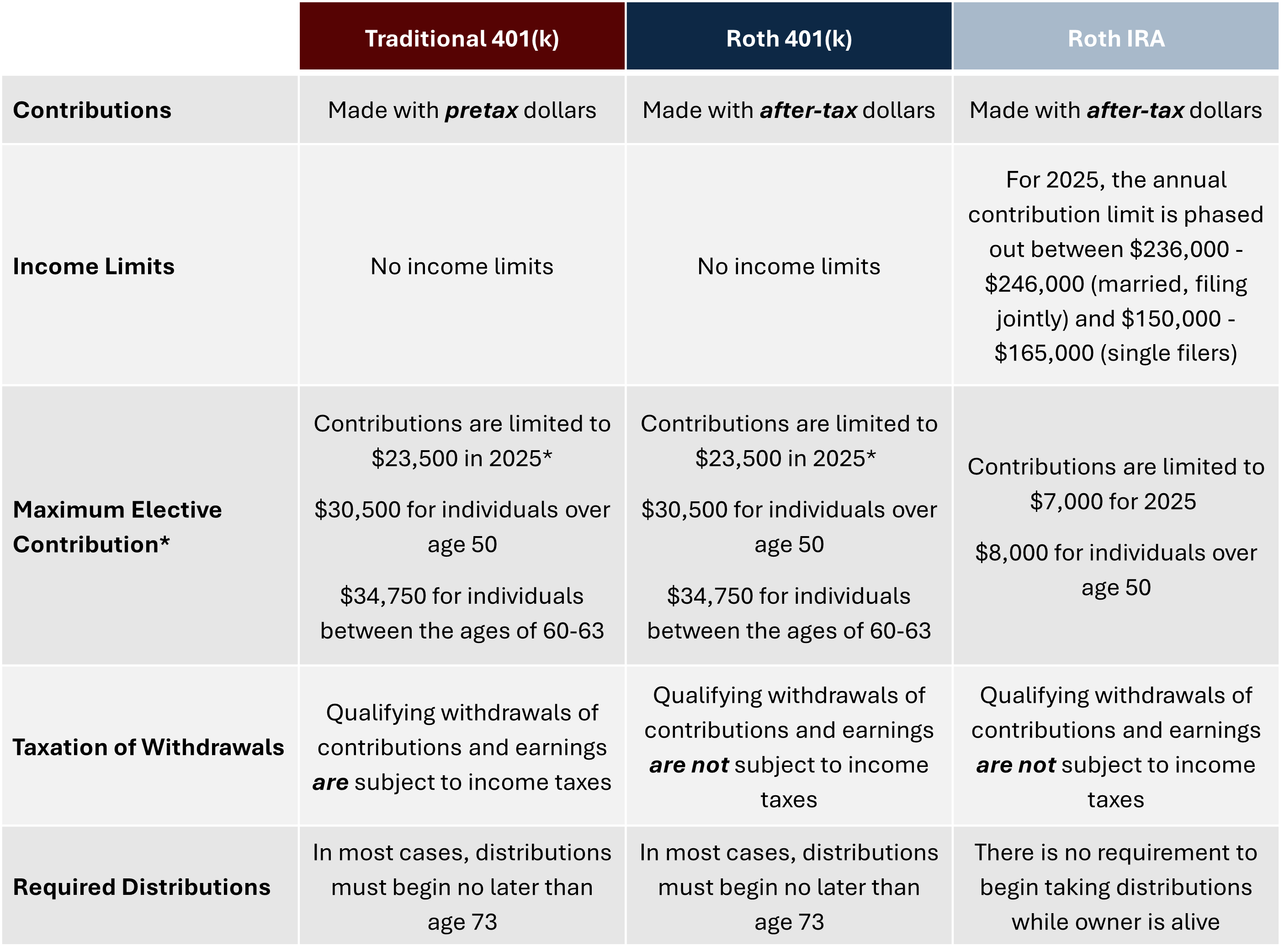

Roth 401(k) plans are subject to the same annual contribution limits as traditional 401(k) plans which is $23,500 for 2025 ($31,000 for those over age 50 or $34,750 for those aged 60-63). It’s important to note that these are cumulative limits that apply to all accounts with a single employer, so you are not able to contribute $23,500 to a traditional 401(k) and an additional $23,500 to a Roth 401(k).4

While your contributions to a Roth 401(k) are made with after-tax money, any matching funds from your employer will be deposited into a separate, pretax account. That means these matching funds will be taxed as ordinary income when withdrawn. Be sure to consider your expected expenses and income sources in retirement. If you anticipate sizable taxable income from other accounts, a Roth 401(k) can help balance your tax obligations more effectively. See the accompanying table below for more information on the differences between accounts.

Taking the Next Step

Savings money for retirement is a key component of a sound financial strategy, but deciding whether to leverage a traditional 401(k) or a Roth 401(k) isn’t always straightforward. Retirement planning involves considering a wide range of factors, including your current income, expected tax rate, and personal goals.

If you’re unsure about the right strategy for you, please feel free to reach out and our team can help you clarify your options and put together a plan that makes sense for you.

*This is an aggregate limit by individual rather than by plan. The total of an individual’s aggregate contributions to his or her traditional and Roth 401(k) plans cannot exceed the deferral limit – $23,500 in 2025 ($31,000 for those over age 50 and $34,750 for those between the ages of 60 and 63).

1To qualify for the tax-free and penalty-free withdrawal of earnings, Roth 401(k) distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawals also can be taken under certain other circumstances, such as a result of the owner’s death or disability. Employer matches are pretax and not distributed tax-free during retirement. Once you reach age 73, you must begin taking required minimum distributions.

2In most circumstances, you must begin taking required minimum distributions from your 401(k) or other defined contribution plan in the year you turn 73. Withdrawals from your 401(k) or other defined contribution plans are taxed as ordinary income, and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

3Roth IRA contributions cannot be made by taxpayers with high incomes. In 2025, the income phaseout limit is $165,000 for single filers, $246,000 for married filing jointly. To qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawals also can be taken under certain other circumstances, such as a result of the owner’s death or disability. The original Roth IRA owner is not required to take minimum annual withdrawals.

4IRS.gov, 2025